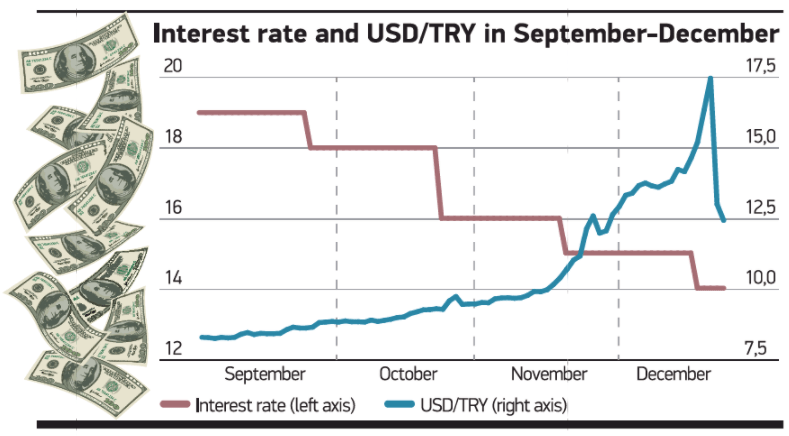

The decline in foreign exchange (FX) rates following the sharp increase have relieved us psychologically. We’ve returned to November levels. The poison entered the structure of prices and the unpoisoning won’t be that easy. Although FX rates were expected to increase when the Central Bank lowered the policy rate, the rate cut was insisted upon. Although costs were expected to increase when FX rates hiked, why were backs turned to this situation? This question will be more frequently asked when the dust settles. Wouldn’t it be better if we performed this operation when USD/TRY saw 12.00-13.00 or even stood at a lower level? Wouldn’t it be better to act so that such an operation wasn’t necessary? Not to touch the Central Bank’s interest rate for instance. Let’s say ‘there is a method’ and look at the current state. Now, we’ve achieved the decline in FX rates, but prices haven’t fallen and aren’t expected to fall at least in the short term. If this implementation receives high demand, if a high number of Foreign Currency Protected TRY Deposit Accounts (KKM) are opened and FX rates increase in the upcoming months especially due to external factors, won’t there be an incalculable burden on the Treasury?