BY TALIP AKTAS

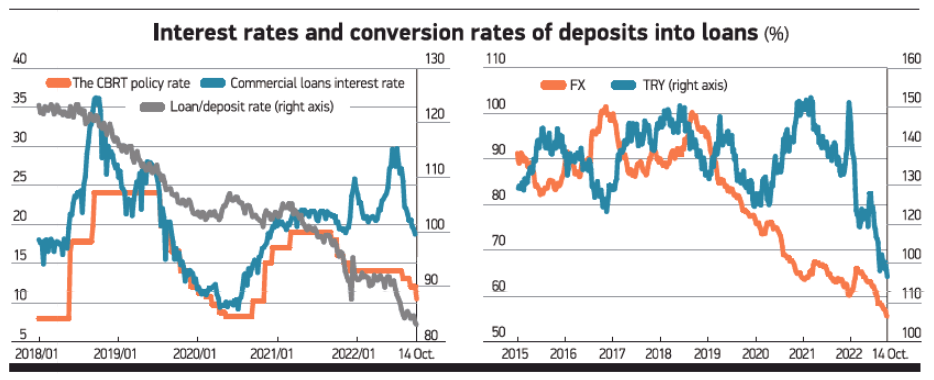

The Central Bank’s rate cuts since September 2021, when inflation began its sharp rise, have limited loan capacity and the conversion rate of deposits to loans has hit a historic low as a result of the ‘hidden’ upper limit for interest rates (IR). Why are borrowers having trouble accessing loans? The direct/indirect upper limit for banks’ loan and deposit IRs and the surge in bond-based required reserves restricted banks’ ability to lend and contracted loan capacity. Deposits (with the impact of the FX rate difference of the FX-protected TRY deposit accounts) have risen by 95% as of mid-October over the past 12 months, while the surge in loans has remained at 68% including renewals, structuring, and FX rate differences. Meanwhile, banks’ securities stocks consisting of primarily Treasury bonds jumped 80% from TRY 1.17tr to TRY 2.2tr. Intervention in banks’ IRs is restricting the private sector’s ability to access loans, while IR cuts are reducing the Treasury’s borrowing cost. The Treasury doesn’t have difficulty in bond borrowing given the record negative IR. The liraization strategy seems to aim to finance record budget deficits estimated at TRY 461bn for 2022 and TRY 660bn for 2023 rather than to prioritize ‘growth’ as stated in the Monetary Policy Committee statements.