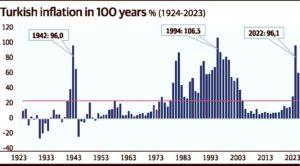

The first graph shows the evolution and average annual inflation over the period 1924-2023. The three highest annual inflation rates and the years in which they occurred are also marked. There is no consumer inflation going back to the early years of the Republic. Instead, the graph shows annual changes in the price index known as the ‘GDP deflator’. It represents the average inflation in any given year. You can roughly think of it as the average of producer inflation and consumer inflation. The average inflation over a hundred years is 23.6 percent.

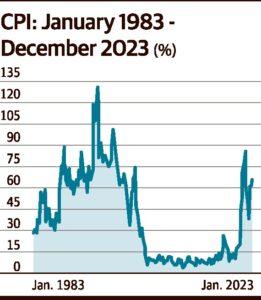

The periods of the Great Depression and the Second World War create a lot of ‘noise’ in the series, in technical terms. Or the signal is too scratchy, as it was in the old days of the old radio. Let me shorten the period: The second graph shows annual consumer inflation and its average for each month between 1983 and 2023. This time the average is higher: 39.3 percent. If these high inflation rates were behind us and we had been living with low single-digit inflation rates for a while, we would just see it as an unpleasant memory of the past. This is not the case. Unfortunately, since 2017, inflation has been in double digits again and has been rising for the last three years. In 2022, the second-highest inflation of the first century (considering yearly averages) is observed.

Why is this so? The short answer is that there is no will to reduce inflation; it is not in the interest of the influential and the authorities. As the agenda permits, I will pursue this question for a while, albeit intermittently. I will discuss why and possibly to what ends the fragilities that spiked inflation in the past were created. I think it will be ‘fun’.

Let me start with the ‘obvious’ one, i.e. the motive of letting markets to rally. Most of the other motives ultimately lead to the desire to increase the growth rate. We mortal economists know well that policies that try to increase the growth rate in a period above the potential growth rate by increasing aggregate demand lead to significant imbalances in the economy. You can raise the growth rate above the potential growth rate for a few years – for example, by having the banks open up credit at full throttle – but the end result will be disappointing. Because inflation and the current account deficit will rise. If domestic demand is accelerated by rapid credit expansion, financial vulnerabilities also increase. After a while, the problems created lead to growth below potential.

In the 1983-2023 period, Turkey’s average GDP per capita growth rate is 3 percent, which can roughly be taken as the potential growth rate. A parenthesis: Our potential growth rate is probably lower now due to the lack of productivity growth in recent years, but there is no precise measurement. Let’s assume 3 percent. The right thing to do is to try to raise the potential growth rate. But if there are elections coming up, who will try to increase the potential? Because it requires long-term work. For example, you need to raise the skill level of the labor force. Who knows how many years it will take. And success is not guaranteed. In this case, it is necessary to start ‘result-oriented’ work as soon as possible.